Tax Reporting

RIT provides students and parents with several documents to support the tax filing process, including the 1098-T, 1098-E and 1042-S.

More information on each of these documents can be found below.

Form 1098-T

The 1098-T Form may assist you in completing IRS Form 8863 – the form used for calculating the education tax credits that a taxpayer may claim as part of your tax return. You also have access to your RIT student account through eServices to obtain detailed account transactions for the calendar year.

RIT is unable to provide you with individual tax advice, but should you have questions, we recommend that you seek the counsel of an informed tax preparer or adviser. For more information about Federal Form 1098-T, see IRS Publication 970.

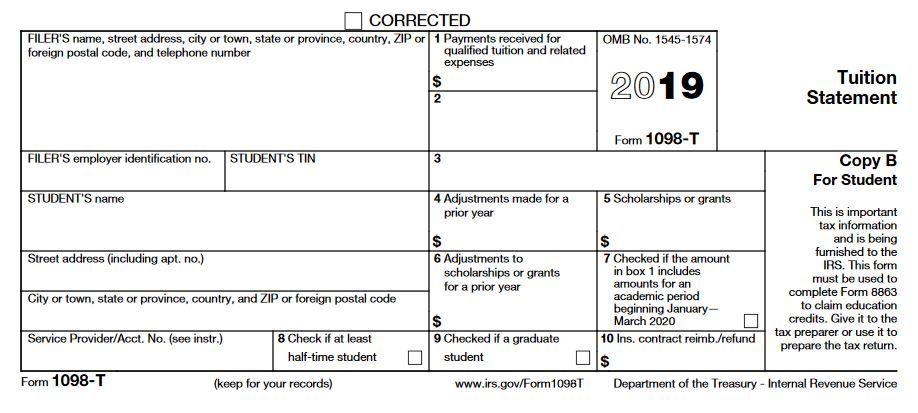

IRS Form 1098-T provides information to students, from educational institutions, which may be used in determining a student’s eligibility for education tax credits.

1098-Ts are processed and mailed by an outside agency, ECSI. The forms are mailed to eligible students before January 31.

Your 1098-T is available on ECSI's web site or by calling ECSI at 866-428-1098. RIT's school code is 02.

Not necessarily; determination of eligibility is the responsibility of the taxpayer.

You or your parents may be eligible for the educational tax credits on your tax return. For more details, refer to IRS Publication 970 or see your tax preparer.

- RIT’s name, address, and taxpayer identification number

- Student’s name, address, and taxpayer identification number

- Whether the student was enrolled in at least half-time or full-time academic workload for at least one academic period

- Whether the student was enrolled exclusively in a graduate-level program

- Amount of qualified tuition and fees paid to RIT during the prior calendar year

- Box 1: The total payments received for qualified tuition and related expenses, less any related reimbursement or refunds.

- Box 2: No Longer Used

- Box 3: No Longer Used

- Box 4: Reimbursements or refunds of qualified tuition and related expenses reported on a prior year Form 1098-T.

- Box 5: The total of all scholarships or grants administered and processed by RIT. The amount of scholarships or grants for the calendar year (including those not reported by RIT) may reduce the amount of any allowable tuition and fees deduction or the education credit you may claim for the year.

- Box 6: Reduction to the amount of scholarships or grants reported on a prior year Form 1098-T.

- Box 7: If this box is checked, the amount in Box 1 included amounts for an academic period beginning in the next calendar year. See IRS Publication 970 for how to report these amounts.

- Box 8: Indicates whether you are considered to be carrying at least one-half the normal full-time workload for your course of study at RIT.

- Box 9: Indicates whether you are considered to be enrolled in a program leading to a graduate degree, graduate-level certificate, or other recognized graduate-level educational credential.

- Box 10: The total amount of reimbursements or refunds of qualified tuition and related expenses made by an insurer. The amount of reimbursements or refunds for the calendar year may reduce the amount of any allowable tuition and fees deduction or education credit you may claim for the year.

Reporting to the IRS depends primarily on your SSN or ITIN. It is very important for you to have the correct information on file with RIT. If RIT does not have an SSN on file, or if your SSN is incorrect, complete and return, in-person, an IRS W-9 form to the RIT Registrar’s Office.

There are multiple reasons why you may not have received a 1098-T:

- If you are classified as a non-resident alien, RIT is not required to produce a 1098-T

- Inaccurate address (i.e., outdated or inaccurate address on file with RIT). If this occurred, you can update your information in your student center and you may access the 1098T at ECSI.

If the payment is received and processed by RIT prior to January 1, 2021, the information will appear on the 2020 Form 1098-T.

The 2020 Form 1098-T will not be changed; however, the following year’s form will report any refund associated with the 2020 payment.

It may or may not be (dependent upon the source of funds). Please refer to IRS Publication 970.

Payments received from a third party are reported in both Box 1 and Box 5. Please speak with a tax adviser for information about how this impacts any potential tax credit, etc.

Tuition waivers will reduce the sum of a student’s QTRE (Qualified Tuition and Related Expenses), therefore, it lowers the total potential tax credit available.

Section 65050S of the Internal Revenue Code, as enacted by the Taxpayer Relief Act of 1997, requires institutions to file information returns to assist taxpayers and the IRS in determining the amount of qualified tuition and related expenses (qualified expenses) for which an education tax credit is allowable under section 25A (American Opportunity and Lifetime Learning Education tax credits), as well as other tax benefits for higher education expenses.

RIT is not able to provide individual tax or legal advice. Please seek advice from the IRS or a tax professional. Information is also available in the IRS Publication 970: Tax Benefits for Education.

You can view payment details in eServices. Your account details are listed by semester in the Semester Summary link.

No; this information will be provided by your loan servicer(s) on Form 1098-E.

Form 1098-E

Form 1098-E reports interest paid on Federal Perkins Loan provides detailed information.

Important: Information regarding immigration, employment, and tax substantial authority are the responsibility of each individual. Please keep in mind that no one from RIT, while in their official role at the university, can act as a tax consultant, give personal, legal, or tax advice, or represent an individual dealing with the Internal Revenue Service. Thus, any assistance the above information may provide is given as a courtesy to you, and as such, should not be construed in any way as the rendering of legal or tax advice.

Form 1042-S

Form 1042-S is a report of tax withheld and is issued to international students that have received scholarships that exceed their tuition and required fees. The form is issued by mid-March.

Students that are U.S. Citizens or permanent residents will not receive a 1042-S.

We are not tax experts. The information we provide is not a substitute for advice from the Internal Revenue Service (IRS) or a qualified tax professional. We cannot address any personal tax questions or file your taxes for you. However, RIT has purchased Sprintax, a tax preparation system to make your tax filing easy. Additional information regarding Sprintax can be found on the International Student Services website.