Lease Classification and Accounting

Purpose

Rochester Institute of Technology adopted the Financial Accounting Standards Board (FASB) new accounting guidance on leases FASB Accounting Standards Codification Section 842 ("ASC 842") on July 1, 2020.

This policy is intended to differentiate the appropriate classification of leases and document authoritative literature for the accounting treatment for leases by the lessee and lessor. The Controller’s Office is responsible for classifying leases in the year of their origination in accordance with the applicable financial accounting guidance. The Controller’s office is also responsible for accounting for all leases during the life of the lease in accordance with the applicable financial accounting guidance.

ASC 842 requires the University to determine whether a contract contains a lease before deciding on the appropriate accounting treatment. If the agreement contains a lease, it must be classified as either an operating or a finance lease and, as lessor a sales-type, direct finance or operating. The appropriate object code must be used for transactions related to the lease. The guidance follows a ‘right of use model’ (ROU) which essentially recognizes a ROU asset and lease liability at inception for all leases with exemption for leases with terms less than 12 months.

Policy

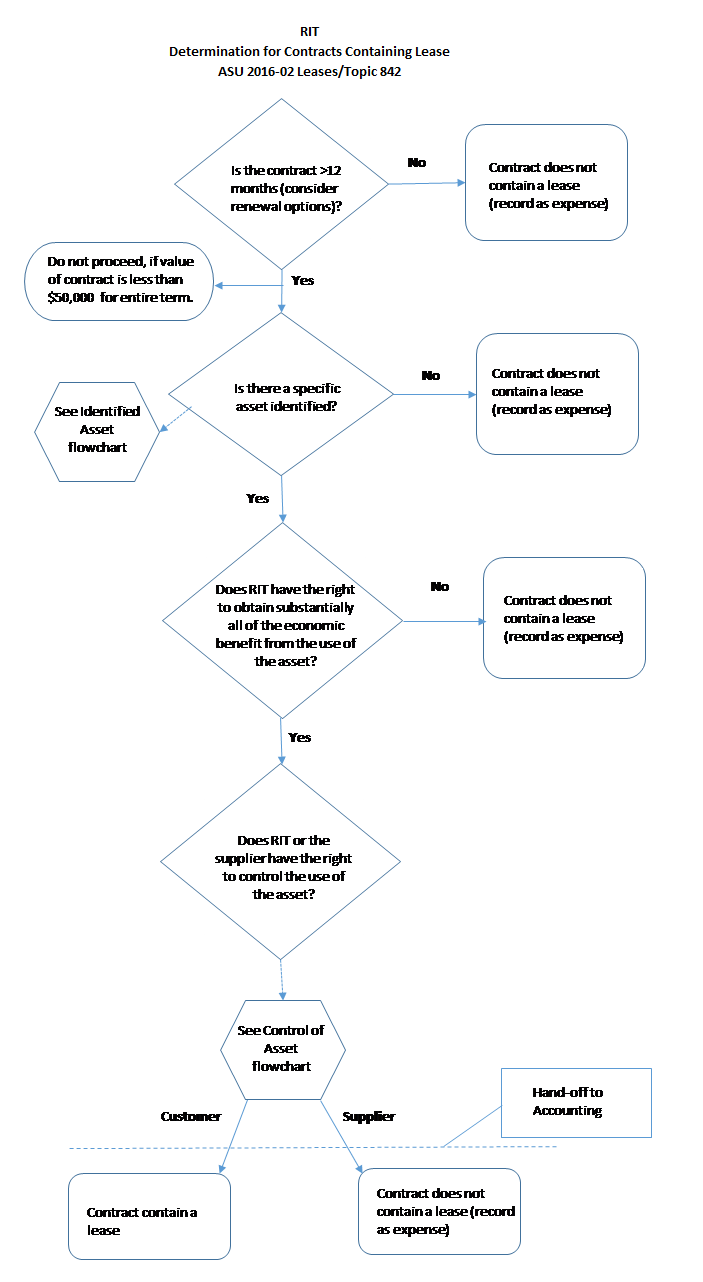

Long-term contracts (terms greater than 12 months) and total lease term value, including more than likely options to extend, of $50,000 or greater, will be assessed using the ASC 842 guidance to determine whether or not there is a lease component.

Lease classification is imperative to properly account for contracts that meet the criteria of Topic 842. The RIT Procurement Services Office (PSO) plays an important role in the lease determination process, as nearly all vendor contracts are executed through PSO. Property Accounting collaborates with PSO in final determination if the contract contains a lease and appropriate classification of the lease. Departments should contact PSO upon initiation of a contract.

Contact Information:

Controller's Office - Property Accounting -> propertyacctg@rit.edu

Controller's Office - Procurement Services Office -> purchsae@rit.edu

Does a Contract Contain a Lease?

Departments should have an understanding of whether a contract contains a lease. The following information summarizes the FASB guidance on determining if a contract contains a lease (both RIT as lessee and lessor).

Definitions:

- Lease - Present when a contract, or part of a contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

Is there a specific asset identified?

- Identified asset - To meet the definition of a lease, an arrangement must require use of an explicitly or implicitly identified asset that is physically distinct.

- Explicitly specified asset - If a contract explicitly specifies the asset to be used (e.g., by serial number or a specified floor of a building), the contract contains an identified asset unless the supplier has substantive substitution rights.

- Implicitly specified asset - A contract that does not explicitly specify an asset to be used to fulfill the contract may implicitly specify the asset, for example, when the asset is made available for use. When only one asset can be used to fulfill the contract (e.g., because of economic or legal factors or because the lessor has only one asset available to perform under the contract) then the asset is considered implicitly specified.

- Physically distinct - An identified asset must be physically distinct. A physically distinct asset may be an entire asset or a portion of an asset. For example, a building is generally considered physically distinct. One floor within the building may also be considered physically distinct if it can be used independent of the other floors (e.g., point of entry or exit, access to lavatories).

- Certain assets may lend themselves to use by more than one party and need to be carefully evaluated to determine if they are physically distinct.

- When thinking about whether an asset is physically distinct, entities may need to consider the nature of the asset and evaluate how the asset was designed to be used.

- A customer can obtain economic benefits from use of an asset directly or indirectly in many ways, such as by using, holding, or subleasing the asset. (ASC 842-10-15-17)

- A customer may derive economic benefits from its use of an asset by producing goods for its own use or resale, providing services, or enhancing the value of other assets. The parties to the contract should consider the economic benefits that can be derived from the use of the asset but not benefits that are derived solely from ownership of the asset (e.g., proceeds from the sale of the asset).

- The right to determine how and for what purpose an asset is to be used is a strong indicator of which party directs the use of the identified asset because such rights determine the economic benefits that can be derived from using the asset during the period of use.

- Identify rights that are most relevant to changing how and for what purpose the asset is used (i.e., those that affect the economic benefits to be derived from the asset)

- Decisions about how and for what purpose an asset will be used are the most relevant factors to consider when assessing which party directs the use of the identified asset. A reporting entity should give the most weight to the factors that have the greatest impact on the economic benefit to be derived from that asset.

- If the supplier has the ability to alter the predetermined decisions, then the customer does not have the right to direct the use of the asset.

Lease Classification (Lessor)

While lessees are now required to record a lease liability and right-of-use asset for all leases, the model applied by lessors depends upon the type of lease. Although lease accounting will not significantly change for most lessors, lessors may experience revenue recognition changes.

A lessor should determine lease classification based on whether the lease represents financing or a sale, as opposed to conveying usage rights, by determining whether the lease transfers substantially all the risks and rewards of ownership of the asset. The lessor should determine at the lease commencement if the lease transfers control of the asset. If there is no transfer of control, no selling profit or revenue should be recognized by the lessor. This is a change from the existing GAAP in that it aligns the concept of sale with the new revenue recognition standard.

Lease Accounting

On the lease commencement date, a lessee is required to measure and record a lease liability equal to the present value of the remaining lease payments, discounted using the rate implicit in the lease using information available at the commencement date (or if that rate cannot be readily determined, the lessee’s incremental borrowing rate). Lease arrangements should be reviewed to ensure that all applicable payments are being considered.

At the commencement date, the cost of the right-of-use asset shall consist of all of the following:

- The amount of the initial measurement of the lease liability

- Any lease payments made to the lessor at or before the commencement date, minus any lease incentives received

- Any initial direct costs incurred by the lessee (as described in paragraphs 842-10-30-9 through30-10).

RIT's Property Accounting team is responsible for preparing the calculations and entries to record the initial lease measurement. Departments will use the following respective accounts to prepare purchase orders or invoice payments.

Finance Lease Accounting

Operating Lease Accounting (lessee)

Sales-Type Lease Accounting (lessor)

Since control of the asset is transferred to the lessee, the lessor should derecognize the leased asset and record the net investment in the lease at lease commencement. Contact Property Accounting if you believe you have such a transaction. They will review and facilitate the preparation of this type of transaction, if applicable.

- The net investment in the lease is the lease receivable plus unguaranteed residual asset, if any, measured at the present value discounted using the rate implicit in the lease.

- The lessor should recognize any profit or loss from the sale of the asset.

- Initial direct costs should be expensed unless the fair value of the asset equals its carrying amount (i.e. no profit or loss). When there is no profit or loss, the initial direct costs should be deferred and recognized over the lease.

Operating Lease (lessor)

Direct Financing Lease (lessor)

Contact Property Accounting if you believe you have such a transaction.

Lease Accounting - Ledger Accounts

The following accounts should be used when creating purchase orders for the respective lease agreements after PSO and Property Accounting have concluded on the treatment of the contract.

| Category | Object Code | Description |

|---|---|---|

| Operating Lease Liability | 38400 | ROU Operating Lease Obligation |

| Finance Lease Liability | 38300 | ROU Finance Lease Obligation |

Property Accounting will manage other accounts associated with the ROU asset and corresponding depreciation and interest (if a finance lease).

Ongoing Requirements

If departments or PSO experience the following scenarios after the lease has been recorded, the lease classification will need to be reassessed and adjustments to values recorded as applicable. Departments should contact PSO or Property Accounting.

- Change in assessment of lessee renewal, termination or purchase options

- Change in amounts probable of being owned under a lessee provided residual value guarantee

- Contingency resolved such that some or all variable payments become fixed

Annually the ROU assets recorded will need to be assessed for impairment by applying the long-lived assets. Departments may be contacted by Property Accounting to inquire about the identified ROU asset.